Market Update: Mon, May 6, 2019

Posted by lplresearch

Daily Insights

Trade tensions escalate again. Just as the headlines suggested a deal was close, President Trump’s threat over the weekend to raise tariff rates on $200 billion of Chinese imports and institute new tariffs on an additional $325 billion of Chinese goods has driven S&P 500 Index futures down more than 1% today. We still expect a deal in fairly short order for several reasons. This action conflicts with the tone of comments out of other key negotiators on both sides, and President Trump has a track record of getting toughest as negotiations near the finish line (NAFTA 2.0 is an example). Also, a deal is clearly in the best interest of both parties (Trump wants re-election and China wants growth). While this threat clearly increases short-term risk, and was a surprise to markets, we believe a path to compromise on using tariffs as an enforcement mechanism—the main sticking point—still exists.

Will “Sell in May and go away” work this year? Every year a barrage of Wall Street commentaries, media stories, and investor questions flood in about this popular stock market adage reflecting the weakest six months of the stock market historically. In our latest Weekly Market Commentary due out later today, we tackle this commonly cited seasonal pattern, and discuss why we may see some seasonal weakness in 2019. While this six-month stretch has seen higher equity prices in recent years, with stocks up significantly from the December lows, some caution may be warranted this year.

The case against a rate cut. The Federal Reserve (Fed) and markets are at odds with each other again. Futures are pricing in more than a 50% chance of a rate cut in 2019, and short-term yields have dropped below the upper-bound Fed funds rate for the first time this cycle. Markets’ concern has centered on slowing inflation, which the Fed has dismissed as a temporary trend. In this week’s Weekly Economic Commentary, we’ll outline the high bar for a rate cut historically, and why a Fed pause makes sense here.

Star Wars and investing. May 4th was Star Wars Day 2019. It comes from a play on words, “May the Force be with you.” Or “May the fourth be with you,” get it? Today on the LPL Research blog we take a fun look at some of the most famous Star Wars quotes in history and what they can tell us about investing.

Earnings turn positive. With 388 S&P 500 companies having reported, S&P 500 earnings growth is tracking to a 0.9% year over year increase for the first quarter, more than 3 percentage points above quarter-end estimates (Refinitiv data). Consumer discretionary and healthcare have produced the biggest upside surprises, healthcare has produced the biggest increase (+9%), while energy sector earnings have fallen by and missed by the most despite the sharp rise in oil prices during the quarter. This week 59 S&P 500 companies will report results.

Estimates still holding up well. Forward estimates for the S&P 500 have only fallen by 0.4% during earnings season, better than average and reflecting the better-than-feared global growth environment. Consensus estimates for 2019 S&P 500 earnings growth currently stand at 3-4%, which we believe is overly pessimistic given positive economic fundamentals and favorable prospects for a U.S.-China trade deal.

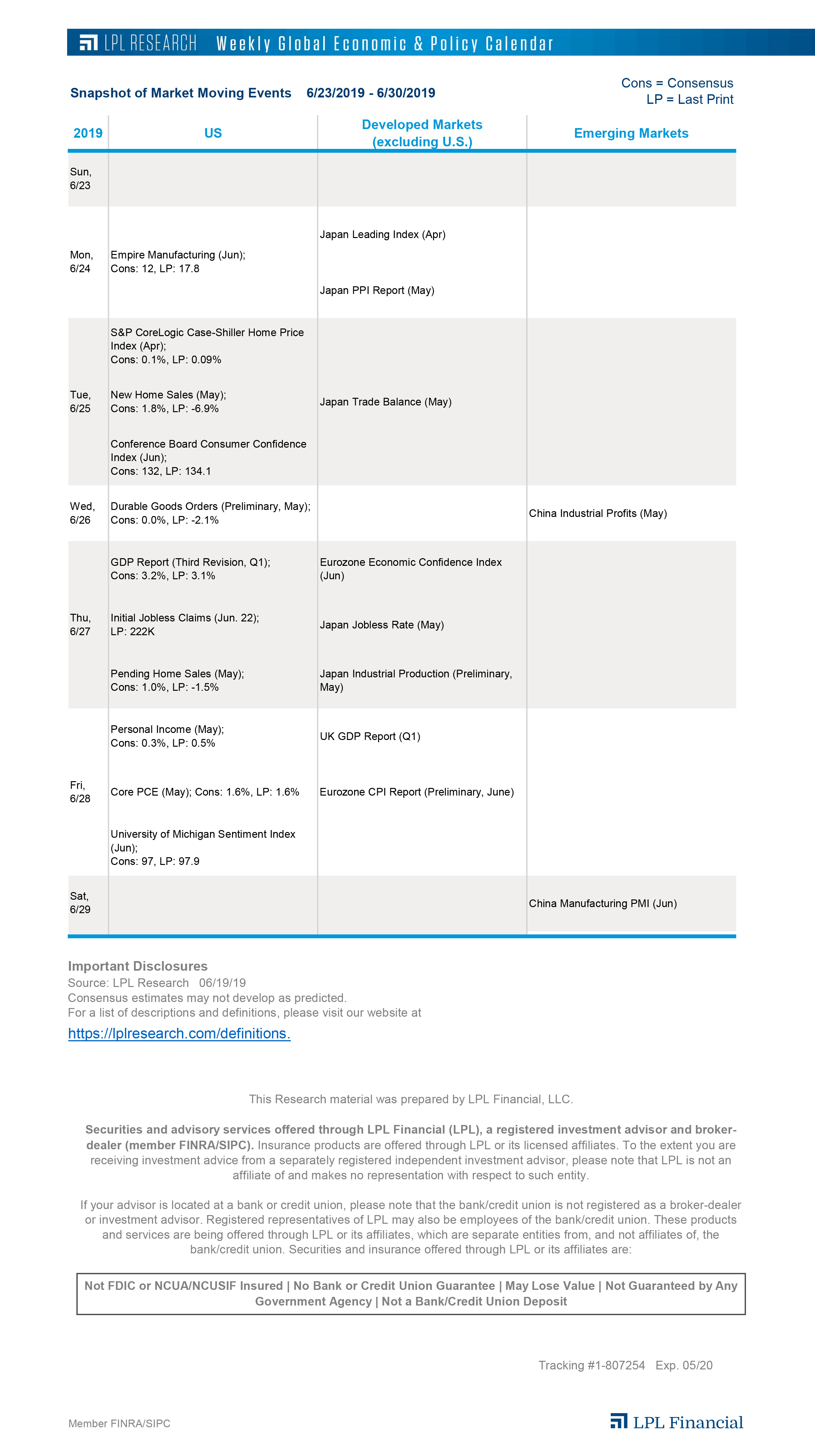

A look ahead. Looking ahead, the steady flow of corporate earnings continues, both in the U.S. and Europe, while U.S. inflation and several important data sets out of China highlight the economic docket. Track these and other important events on our Weekly Global Economic & Policy Calendar.

Click Here for our detailed Weekly Economic Calendar

Monday

- Markit Germany Services PMI (Apr)

- Markit Eurozone Services PMI (Apr)

- Eurozone Retail Sales (Mar)

- Nikkei Japan Manufacturing PMI (Apr)

Tuesday

- JOLTS Job Openings Report (Mar); LP: 7,087

- Nikkei Japan Services PMI (Apr)

- China Trade Balance (Apr)

- China Exports (Apr)

- China Imports (Apr)

Wednesday

- Germany Industrial Production (Mar)

- China Trade Balance (Apr)

- China Exports (Apr)

- China Imports (Apr)

- China CPI Report (Apr)

- China PPI Report (Apr)

Thursday

- PPI Report (MoM, Apr); Cons: 0.2%, LP: 0.6%

- Initial Jobless Claims (May 4); LP: —

- Trade Balance (Mar); Cons: -$52B, LP: -$49.4B

- Japan Consumer Confidence Index (Apr)

Friday

- CPI Report (MoM, Apr); Cons: 0.4%, LP: 0.4%

- Monthly Budget Statement (Apr); Cons: $165B, LP: -$146.9B

- Germany Exports (Mar)

- Germany Imports (Mar)

- UK GDP Report (Preliminary, Q1)

- China Foreign Direct Investment (Apr)

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. The economic forecasts set forth in this material may not develop as predicted.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

All company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All performance referenced is historical and is no guarantee of future results.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

The investment products sold through LPL Financial are not insured deposits and are not FDIC/NCUA insured. These products are not Bank/Credit Union obligations and are not endorsed, recommended or guaranteed by any Bank/Credit Union or any government agency. The value of the investment may fluctuate, the return on the investment is not guaranteed, and loss of principal is possible.

Index data obtained via FactSet

{kind=link}