Strength, Growth, and Tension

Weekly Update – June 11, 2018

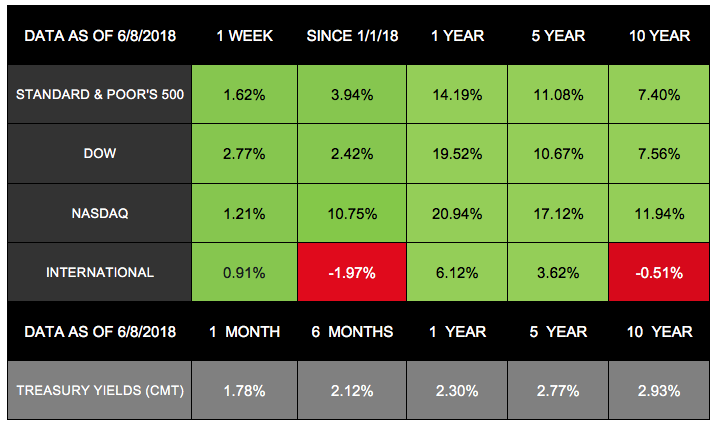

As last week ended, tension between the U.S. and some of its greatest allies was on the rise. Trade remained a hot-button topic ahead of the G-7 meeting in Canada, but investors seemed largely unfazed by the drama.[1] In fact, all 3 domestic indexes posted strong results: The S&P 500 added 1.62% and the NASDAQ gained 1.21%, with both indexes notching their 3 rd week of gains in a row.[2]The Dow ended Friday up 2.77% for the week – recording both its highest level and largest weekly gain since March.[3] International stocks were also up, with the MSCI EAFE increasing by 0.91%.[4]

While geopolitical headlines keep unfolding, new data continues to indicate that the U.S. economy is on solid ground. Let’s examine a few updates we received last week:

- 1 pound beef sirloin

- 8 ounces green beans

- ¼ cup Thai green curry paste

- 1 13.5-ounce can of unsweetened light coconut milk

- 1 8-ounce can of bamboo shoots

- Cut the beef into thin slices. Add ¼ teaspoon kosher salt to season.

- Heat a large skillet on medium-high. Spread 1 tablespoon of olive oil on heated skillet. Cook the beef in the skillet until it is browned, 2-3 minutes on each side. Move to a plate.

- As the beef cooks, cut the green beans in half. Hold for later.

- Put the Thai green curry paste into the skillet and stir while cooking, 2 minutes.

- Stir in the unsweetened light coconut milk. Bring the mix to a simmer.

- Put the green beans into the skillet and cook until the beans are tender, 3-5 minutes.

- At the same time, pour out the liquid from the can of bamboo shoots.

- Put the beef and the bamboo shoots in the skillet, and thoroughly heat.

- Serve the dish over cooked rice. Sprinkle it with fresh basil.

Recipe adapted from Good Housekeeping[10]

Don’t Say This to Beginner Golfers

You’re taking your friend for his first golf game. You’ve provided a few tips and some basic golf instruction. The beginner has spent time at the range. You’ve been golfing for years, but you’ve never actually taught another player.

- “Keep your head down.”

- “Keep your eye on the ball.”

- “Straighten your left arm.”

- “Keep your head still.”

- “Pause at the top.”

- “Swing slower.”

- Is your home a good fit? Is your monthly power bill less than $100? Winterizing your home might be a better bet.

- Do the math. Check with local providers to determine initial costs.

- How about those incentives and rebates? Do research on federal and state incentives. Rebates can reduce upfront costs by nearly 50%.

- Read the fine print. Before signing a contract with solar PV installers, check the warranties on parts and accessories. After all, you’re in this for the long haul.

- Where does the sun shine? Does your roof get adequate exposure? Shade from trees may block access to the sun’s rays and heat.

- Check out leasing companies. Going solar can be a big initial investment. In many states, some companies can install PVs for no money down. Visit https://www.energysage.com/solar/financing/companies/ for more information.

Portage, MI 49024

269-978-0238

zack.alkhamis@lpl.com

http://www.retirementwealthmanagementgroup.com

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indices from Europe, Australia, and Southeast Asia.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

These are the views of Platinum Advisor Strategies, LLC, and not necessarily those of the named representative,

Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

By clicking on these links, you will leave our server, as the links are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] www.marketwatch.com/story/dow-futures-slide-130-points-as-g-7-leaders-feud-over-trade-2018-06-08

[10] www.goodhousekeeping.com/food-recipes/easy/a47888/thai-beef-and-veggie-stir-fry-recipe/

[11] www.irs.gov/newsroom/multimedia-center